Blockchain Technology Revolutionizing Digital Transactions

As we step into 2026, blockchain technology continues to redefine the digital landscape across industries. From finance and supply chain management to healthcare and entertainment, this revolutionary technology has emerged as a cornerstone for secure, transparent, and decentralized systems. Unlike traditional databases, blockchain operates as a distributed ledger that maintains immutable records of transactions, ensuring both trust and efficiency. Its potential goes far beyond cryptocurrencies like Bitcoin and Ethereum, with enterprises, governments, and startups alike exploring innovative applications to solve complex problems.

Blockchain technology combines cryptography, peer-to-peer networking, and consensus mechanisms to deliver a system where data integrity is verifiable and resistant to tampering. Its ability to decentralize control while enhancing transparency is transforming conventional business models, offering new levels of security and operational efficiency. As adoption grows, understanding the fundamental principles, benefits, and challenges of blockchain technology becomes crucial for individuals and organizations looking to stay ahead in the digital era.

What Is Blockchain Technology?

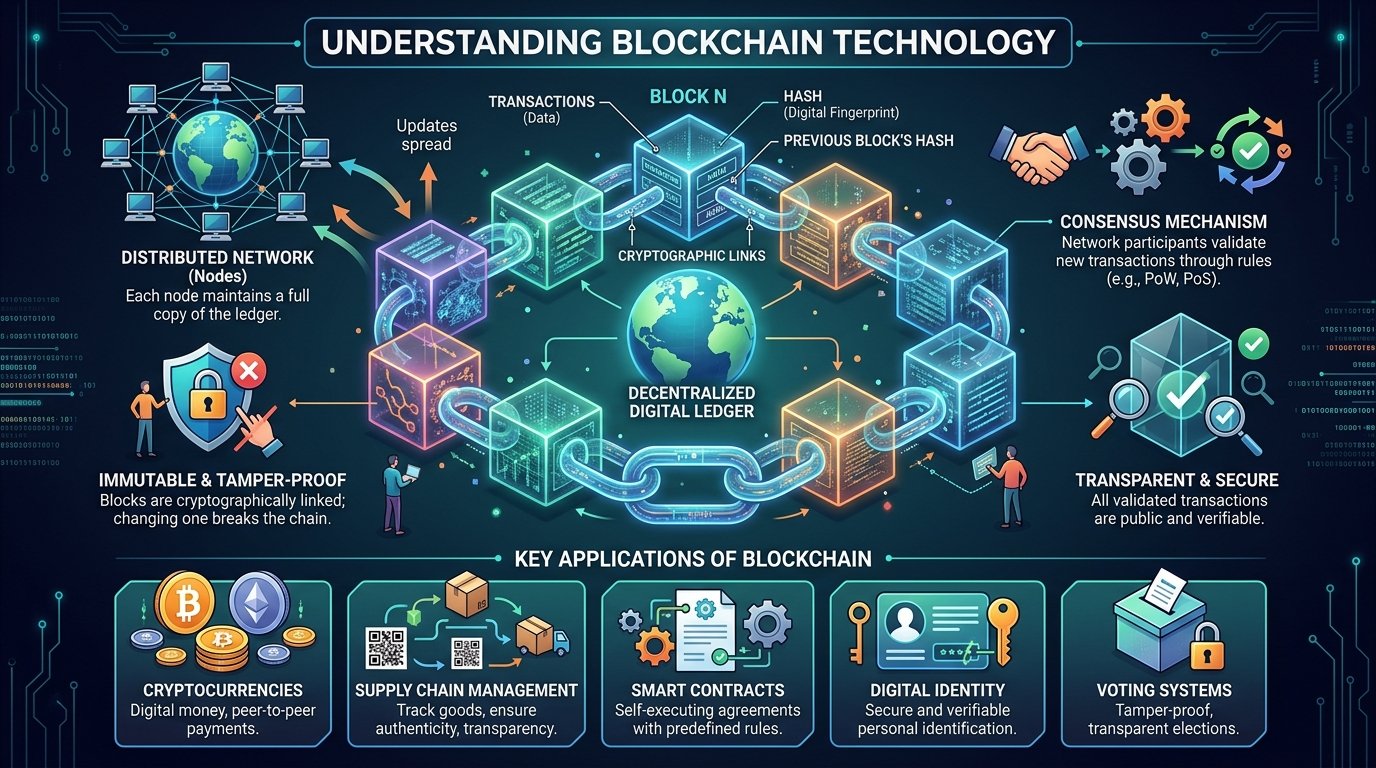

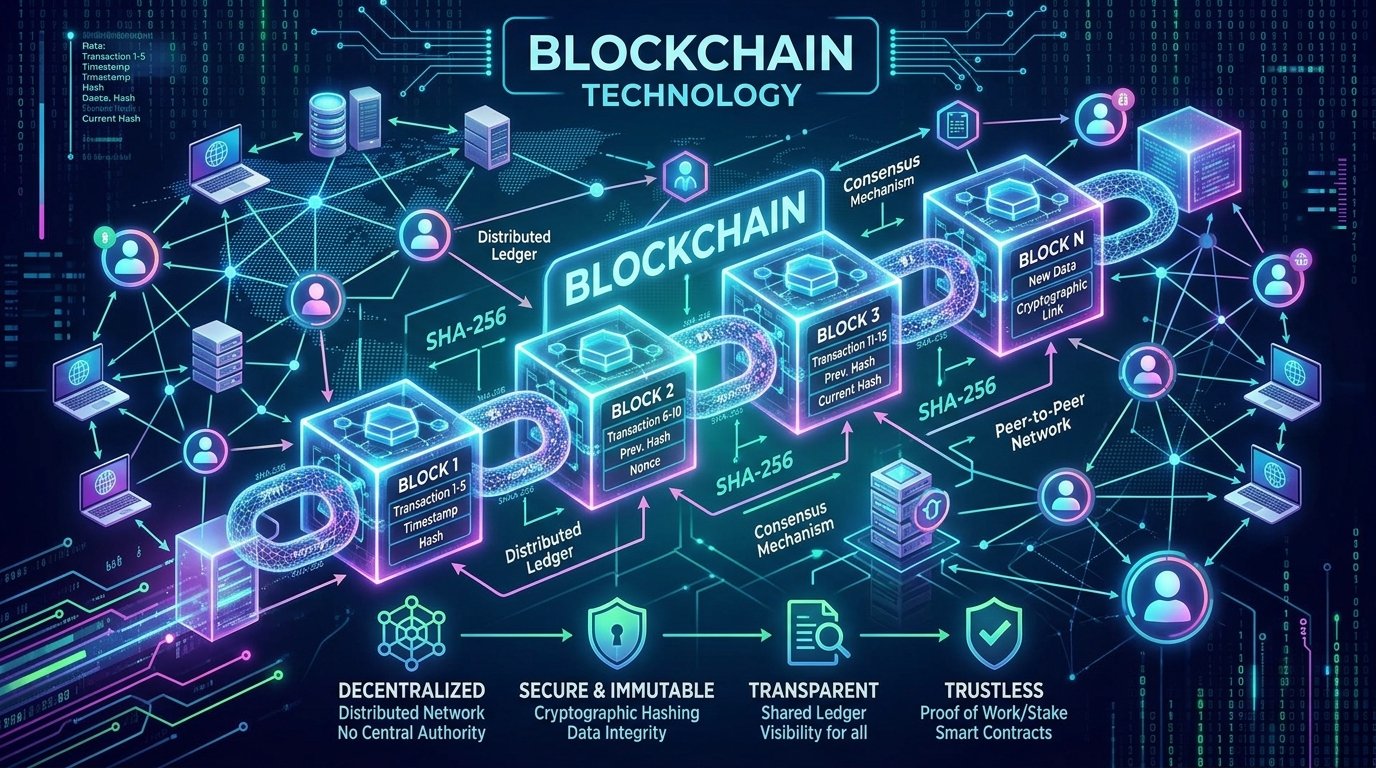

Blockchain technology is a digital ledger system that records transactions across multiple computers in such a way that the registered entries cannot be altered retroactively. This ensures data security, integrity, and transparency. At its core, a blockchain consists of blocks, each containing a batch of transactions. These blocks are linked together chronologically using cryptographic hashes, forming an immutable chain.

Unlike centralized systems controlled by a single authority, blockchain operates on a decentralized network of nodes. Each node maintains a copy of the entire ledger, validating and verifying transactions through consensus mechanisms like Proof of Work (PoW) or Proof of Stake (PoS). This decentralized architecture eliminates the need for intermediaries, reduces the risk of fraud, and ensures that all participants have access to the same reliable information.

The innovation of blockchain technology lies in its combination of decentralization, transparency, and security. These features make it a transformative tool for industries that rely heavily on trust and verification, such as banking, logistics, healthcare, and government services.

How Blockchain Works

Understanding how blockchain works is key to appreciating its potential impact. Each transaction on a blockchain is verified by multiple nodes in the network. Once consensus is reached, the transaction is grouped with others into a block. Each block contains a cryptographic hash of the previous block, forming a chain that cannot be altered without the consent of the majority of the network.

Smart contracts are another essential feature of blockchain technology. These self-executing contracts automatically enforce predefined rules and agreements between parties. By eliminating manual intervention and the need for intermediaries, smart contracts enhance efficiency and reduce the likelihood of disputes.

Moreover, blockchain networks can be public, private, or hybrid, depending on the intended use case. Public blockchains, like Bitcoin, allow anyone to participate and verify transactions. Private blockchains, however, restrict access to specific participants, making them suitable for enterprise-level applications where privacy and control are critical. Hybrid blockchains combine the best of both worlds, offering transparency while maintaining selective access.

Applications of Blockchain Technology

Blockchain technology has evolved far beyond its origins in cryptocurrency, finding applications across a wide range of industries.

Financial Services

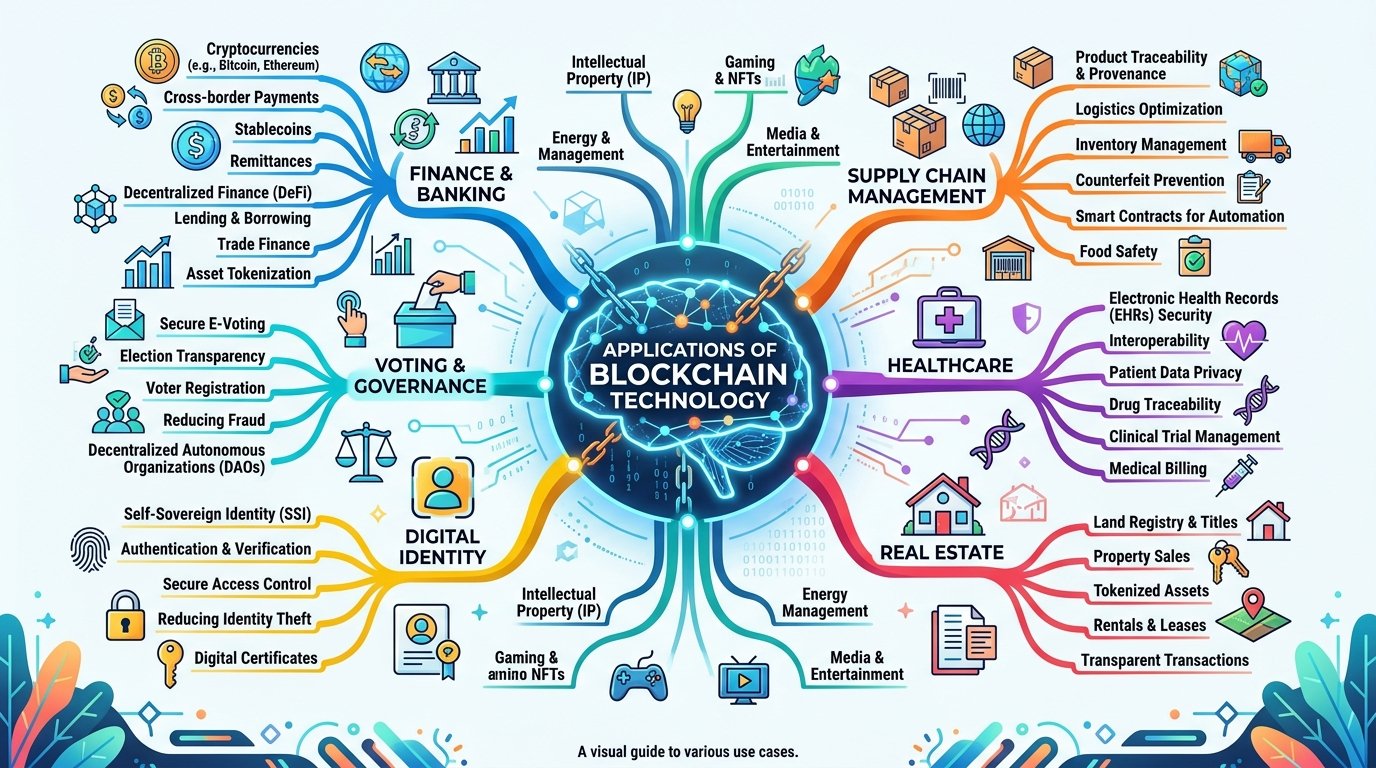

In financial services, blockchain technology has revolutionized how transactions are processed and recorded. Banks and fintech companies are leveraging blockchain to facilitate faster, cheaper, and more secure cross-border payments. Traditional banking systems often involve multiple intermediaries, leading to delays and high fees. Blockchain enables near-instantaneous transactions with minimal overhead, significantly improving efficiency and reducing costs.

Additionally, decentralized finance (DeFi) platforms are creating a new paradigm for financial services. These platforms allow individuals to access lending, borrowing, and investment opportunities without relying on centralized institutions. By removing intermediaries, blockchain technology empowers users with greater control over their financial assets while enhancing transparency and accountability.

Supply Chain Management

The supply chain industry has embraced blockchain technology to enhance transparency, traceability, and efficiency. Every stage of the supply chain, from manufacturing to delivery, can be recorded on a blockchain ledger. This enables companies to track products in real-time, verify authenticity, and prevent fraud.

For example, in the food industry, blockchain can trace the journey of produce from farm to table, ensuring quality and safety. Similarly, in the luxury goods sector, blockchain helps authenticate high-value products, reducing counterfeit risks. By providing a verifiable record of every transaction, blockchain fosters trust between suppliers, retailers, and consumers.

Healthcare

Blockchain technology is transforming healthcare by providing secure, interoperable, and tamper-proof medical records. Patient data can be stored on a blockchain, accessible only to authorized medical professionals. This ensures privacy while allowing seamless sharing of information across hospitals, clinics, and laboratories.

Moreover, blockchain can enhance drug supply chain management, ensuring that medications are authentic and safely delivered to patients. Clinical trials also benefit from blockchain, as data integrity and traceability are critical for validating results. By improving security, transparency, and efficiency, blockchain technology is shaping the future of healthcare delivery.

Real Estate

The real estate industry is leveraging blockchain technology to simplify property transactions, reduce fraud, and enhance transparency. Traditionally, property deals involve extensive paperwork, intermediaries, and verification processes. Blockchain allows property records to be digitized and stored securely, enabling instant verification of ownership and transaction history.

Smart contracts facilitate automated execution of property agreements, eliminating delays and reducing costs. Blockchain also opens the door for fractional property ownership, allowing multiple investors to hold shares in a property. This democratizes real estate investment and increases liquidity in the market.

Voting Systems

Blockchain technology offers a secure, transparent, and tamper-proof solution for voting systems. By recording votes on a blockchain ledger, election authorities can ensure accuracy and prevent fraud. Voters can verify that their vote was counted without revealing their identity, enhancing trust in the democratic process.

Several pilot projects worldwide are exploring blockchain-based voting systems for local and national elections. While challenges remain, including accessibility and scalability, blockchain presents a promising avenue for secure and transparent elections.

Benefits of Blockchain Technology

The widespread adoption of blockchain technology is driven by its numerous benefits.

Security

Blockchain’s decentralized structure and cryptographic algorithms make it highly secure. Altering a record requires control over the majority of the network, making hacking attempts nearly impossible. This level of security is especially valuable for industries handling sensitive data, such as finance and healthcare.

Transparency

Every transaction on a blockchain is recorded and visible to all network participants, ensuring full transparency. This reduces the likelihood of fraud and enhances accountability. Businesses can build trust with consumers, partners, and regulators by demonstrating transparent operations.

Efficiency

Blockchain technology streamlines processes by eliminating intermediaries and automating verification through consensus mechanisms and smart contracts. This reduces delays, operational costs, and human error, leading to more efficient and reliable systems.

Decentralization

By distributing control across a network of nodes, blockchain technology reduces reliance on central authorities. This decentralized model mitigates risks associated with single points of failure and enables more resilient systems.

Challenges and Limitations

Despite its benefits, blockchain technology faces several challenges.

Scalability

As blockchain networks grow, maintaining speed and efficiency becomes challenging. High transaction volumes can lead to congestion and slower processing times. Solutions like layer-2 scaling and sharding are being developed to address these issues, but scalability remains a concern.

Energy Consumption

Proof of Work (PoW) blockchains, in particular, consume significant amounts of energy due to complex computational requirements. This environmental impact has sparked debates and encouraged the adoption of more energy-efficient consensus mechanisms like Proof of Stake (PoS).

Regulatory Uncertainty

Blockchain technology operates in a relatively new regulatory environment. Governments worldwide are exploring frameworks to govern its use, particularly in finance and data privacy. Regulatory uncertainty can hinder adoption and create legal challenges for businesses implementing blockchain solutions.

Interoperability

Different blockchain platforms often operate in isolation, limiting the ability to share data across networks. Interoperability solutions are being developed to enable seamless communication between blockchains, but widespread adoption is still in progress.

The Future of Blockchain Technology

The future of blockchain technology is promising, with continued innovation and adoption across industries. As more organizations recognize the value of secure, transparent, and decentralized systems, blockchain is expected to play a central role in digital transformation.

Emerging trends include the integration of blockchain with artificial intelligence (AI), Internet of Things (IoT), and cloud computing to create intelligent, automated, and interconnected systems. Decentralized finance (DeFi), non-fungible tokens (NFTs), and blockchain-based identity solutions are also likely to see significant growth.

Furthermore, regulatory frameworks are expected to mature, providing clarity and fostering confidence in blockchain adoption. As scalability, energy efficiency, and interoperability challenges are addressed, blockchain technology is poised to become a foundational element of the global digital economy.

Conclusion

Blockchain technology has evolved from a foundation for cryptocurrencies to a transformative tool across multiple industries. Its ability to provide secure, transparent, and decentralized solutions makes it a game-changer for finance, healthcare, supply chains, real estate, and beyond. While challenges such as scalability, energy consumption, and regulatory uncertainty persist, ongoing innovation continues to unlock the potential of blockchain.

As we move further into 2026, embracing blockchain technology offers opportunities for individuals, businesses, and governments to enhance trust, efficiency, and security in the digital age. Understanding its principles, applications, and future potential is essential for those seeking to leverage this revolutionary technology to drive growth and innovation.

FAQs

1. What is blockchain technology in simple terms?

Blockchain technology is a secure, decentralized ledger system that records transactions across multiple computers. Once recorded, these transactions cannot be altered, ensuring transparency and trust.

2. How is blockchain different from traditional databases?

Unlike centralized databases controlled by a single entity, blockchain operates on a decentralized network where each participant maintains a copy of the ledger. This enhances security, transparency, and resilience.

3. Can blockchain be used beyond cryptocurrencies?

Yes. Blockchain technology is applied in finance, supply chain management, healthcare, real estate, voting systems, and many other industries to improve efficiency, security, and transparency.

4. What are smart contracts in blockchain?

Smart contracts are self-executing digital agreements stored on a blockchain. They automatically enforce the terms of a contract, reducing the need for intermediaries and minimizing disputes.

5. What challenges does blockchain technology face?

Key challenges include scalability, high energy consumption (especially for Proof of Work networks), regulatory uncertainty, and limited interoperability between different blockchain platforms.

1 comment